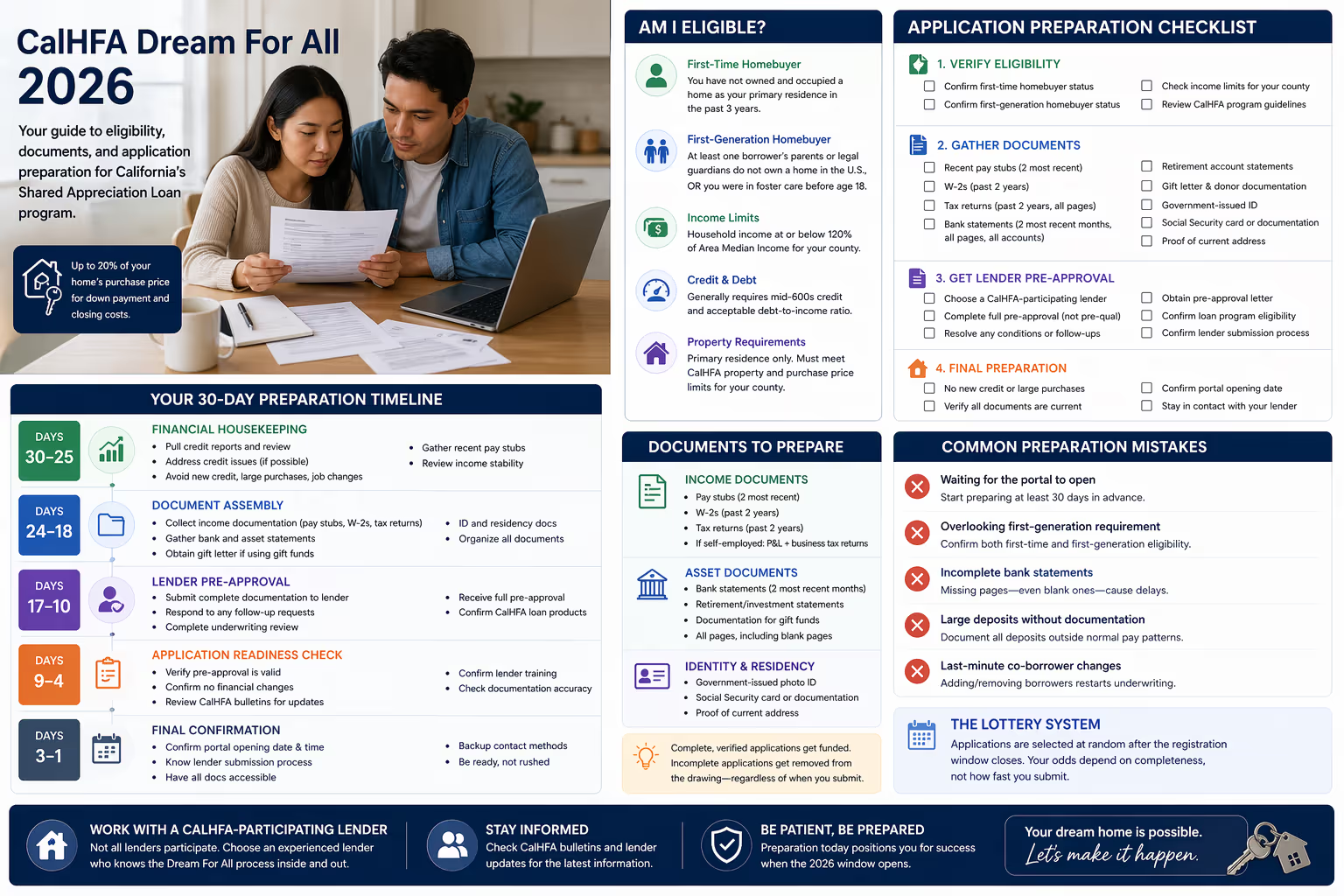

California's Dream For All Shared Appreciation Loan program is expected to return in 2026—and if past funding rounds have taught us anything, it's that preparation separates applicants who get funded from those who don't.

Previous rounds have exhausted hundreds of millions of dollars in days, sometimes hours. [1] The randomized drawing system now used means speed alone won't get you funded. What matters is whether your application is complete, verified, and lender-approved before the registration window even opens.

I've worked with first-time buyers in the Sacramento area who've navigated this process successfully, and the pattern is consistent: the ones who secure funding aren't necessarily faster—they're more prepared. They've done the work weeks in advance, so when the portal opens, their package is already locked in.

This guide covers exactly what to prepare, when to prepare it, and how to position yourself for the strongest possible application when the 2026 lottery window arrives.

How the Dream For All Program Works

The California Housing Finance Agency (CalHFA) designed Dream For All as a shared appreciation loan to help first-time homebuyers cover down payment and closing costs. Unlike traditional down payment assistance grants, this program operates as a second mortgage with a unique repayment structure. [2]

CalHFA provides up to 20% of your home's purchase price (capped at specific limits based on your area's median income). In exchange, when you eventually sell, refinance, or transfer the home, you repay the original loan amount plus a share of your home's appreciation. [2]

How Shared Appreciation Actually Works

The "shared appreciation" piece confuses a lot of buyers, so let's walk through a concrete example.

Say you purchase a home for $500,000 and receive $100,000 in Dream For All assistance (20% of the purchase price). Ten years later, you sell the home for $650,000—a $150,000 appreciation gain.

At sale, you'd owe CalHFA the original $100,000 loan amount plus a percentage of that $150,000 appreciation. The exact percentage depends on your income bracket at the time of the original loan:

Borrowers at higher income tiers (closer to 120% of Area Median Income) typically owe a larger share of appreciation—often matching the original assistance percentage.

Lower-income borrowers may qualify for reduced appreciation shares, sometimes as low as 15% of the gain.

In our example, if you owed 20% of the appreciation, that's $30,000 in shared appreciation on top of the $100,000 principal—$130,000 total repayment. Your lender will provide exact terms during application, as these percentages can shift between funding rounds. [2]

Key Program Features

Loan amount: Up to 20% of purchase price for qualifying borrowers

First mortgage requirement: Must pair with a CalHFA first mortgage loan

Occupancy: Primary residence only; owner-occupancy required

Repayment trigger: Sale, refinance, transfer, or payoff of first mortgage

The program targets households earning at or below 120% of Area Median Income, with enhanced assistance sometimes available for lower-income applicants. [3]

Eligibility Signals: Do You Qualify?

Before investing hours in preparation, confirm you meet the fundamental eligibility requirements. CalHFA publishes detailed guidelines, but these core criteria determine whether you should proceed. [3]

First-Time Homebuyer Definition

CalHFA uses the federal definition: you haven't owned and occupied a home as your primary residence in the past three years. [3] This includes:

Never-before homeowners

Previous homeowners who sold more than three years ago

Individuals who owned property but never occupied it as a primary residence

If you owned a home with a spouse but are now divorced and haven't owned since, you may still qualify—confirm your specific situation with a participating lender.

First-Generation Homebuyer Requirement

Starting with recent funding rounds, CalHFA added a critical eligibility layer: at least one borrower must be a first-generation homebuyer. [3]

You qualify as a first-generation homebuyer if:

Your parents or legal guardians do not currently own a home in the United States, OR

You were in foster care at any point before age 18

This requirement exists alongside the first-time homebuyer rule—you must meet both. Many applicants who qualify as first-time buyers are surprised to learn they don't meet the first-generation criteria because a parent currently owns property.

This is one of the most common disqualifiers. Before you proceed with lender preparation, confirm your first-generation status. If you're unsure whether a parent's property ownership affects your eligibility, discuss the specifics with a CalHFA-participating lender early.

Income Limits

Income limits vary by county and household size. CalHFA typically sets these at 120% of Area Median Income (AMI) for your area. [3]

How to check your county's limits: CalHFA publishes income limit charts organized by county and household size. For Sacramento County and surrounding areas, these limits adjust annually based on HUD calculations. You can find the current limits in the CalHFA income limits PDF on their website or through your participating lender. [3]

Critical detail: Lenders calculate qualifying income based on all borrowers on the loan application, not just the primary earner. If you're applying with a spouse or co-borrower, both incomes count toward the limit.

Credit and Debt Requirements

While CalHFA doesn't publish a single minimum credit score, their first mortgage products typically require scores in the mid-600s range with acceptable debt-to-income ratios. [4] Your participating lender will confirm exact requirements during pre-approval.

Property Requirements

Eligible properties include: Single-family homes Condominiums Townhouses Manufactured homes

Single-family homes

Condominiums (must be on CalHFA's approved list)

Manufactured homes meeting specific standards

Purchase price limits apply and vary by county. Properties must serve as your primary residence—no investment properties or second homes qualify. [3]

Understanding the Lottery System

Dream For All moved to a randomized drawing (lottery) format after previous first-come-first-served rounds saw funding exhausted within minutes. [1] The lottery system fundamentally changes how you should approach the application.

How the Drawing Works

When the application portal opens, eligible applicants submit during a defined registration window—typically lasting several days. After the window closes, CalHFA conducts a randomized drawing to determine the order applications are processed. [5]

Your position in the queue depends entirely on random selection—not how quickly you submitted. However, incomplete or ineligible applications get removed from consideration regardless of lottery position.

The critical insight: Speed doesn't matter. Completeness does. An application missing required documentation gets disqualified whether you submitted in the first five minutes or the last five hours of the registration window.

What the Lottery Means for Your Strategy

Because selection is randomized, your preparation focus shifts from "be fastest" to "be fully ready." A complete, verified, lender-approved application submitted on day three of the registration window has identical odds to one submitted in the first hour.

The applicants who succeed are those whose packages require zero follow-up, zero corrections, and zero additional documentation requests.

The 30-Day Preparation Timeline

Starting 30 days before the anticipated portal opening gives you adequate time to gather documents, complete lender pre-approval, and address any issues that could disqualify your application.

Days 30–25: Financial Housekeeping

Your first priority is stabilizing your financial picture and gathering baseline documentation.

Credit review:

Pull your credit reports from all three bureaus at AnnualCreditReport.com

Document any concerns (late payments, collections, disputes) and determine if you can address them before the window

Avoid opening new credit accounts, making large purchases, or changing jobs if possible

Income documentation (start gathering now):

Recent pay stubs

Tax returns

W-2 forms

CalHFA-approved lenders will need to verify stable employment and income. Major changes during this period—job switches, large deposits, new debts—create verification delays that can derail your application. [4]

Days 24–18: Documentation Assembly

Compile every document your lender will need for pre-approval. Having these ready in advance prevents scrambling during the registration window.

Income documentation:

Two most recent pay stubs (all borrowers)

W-2 forms from the past two years

Federal tax returns (past two years, all pages including schedules)

If self-employed: two years of business tax returns plus year-to-date profit/loss statement

Asset documentation:

Two most recent months of bank statements (all pages, all accounts)

Retirement account statements (if using for reserves)

Documentation for any gift funds (gift letter template available from lender)

Identity and residency:

Government-issued photo ID

Social Security card or documentation

Current address verification (utility bill, lease agreement)

Days 17–10: Lender Pre-Approval

This is where most unprepared applicants fall behind. You need full pre-approval—not just pre-qualification—from a CalHFA-participating lender before the portal opens.

Pre-approval vs. pre-qualification: Pre-qualification involves a surface-level review of your finances. Pre-approval requires document verification, credit analysis, and underwriting review. For Dream For All, you want the full pre-approval completed in advance.

CalHFA maintains a list of approved lenders authorized to originate Dream For All loans. [4] Not every mortgage lender participates—confirm your lender's CalHFA status before proceeding.

During this phase:

Submit complete documentation to your chosen lender

Complete any follow-up requests promptly (missing pages, clarification letters)

Obtain a pre-approval letter specifying CalHFA loan products

Confirm your lender's process for submitting Dream For All applications

Days 9–4: Application Readiness Check

With pre-approval in hand, verify all components are portal-ready.

Final verification checklist:

Confirm your pre-approval remains valid and hasn't expired

Verify no financial changes have occurred that would affect qualification

Review CalHFA's current bulletin for any last-minute program updates [5]

Confirm your lender has received training on the current Dream For All submission process

Common disqualifiers to avoid in this window:

Large unexplained deposits (even if legitimate)

New credit inquiries or accounts

Employment changes without documentation

Co-borrower additions after pre-approval

Days 3–1: Final Confirmation

In the final days before the portal opens:

Confirm the exact portal opening date and time

Verify your lender's submission timeline and whether they batch applications

Have all documentation accessible (digital copies organized by category)

Prepare backup contact methods for your lender during the registration window

Working With a Participating Lender

Your lender relationship may be the most important factor in Dream For All success. CalHFA doesn't accept direct applications—everything flows through participating lenders who then interface with the agency. [4]

Choosing the Right Lender

Not all participating lenders have equal experience with CalHFA products. When interviewing lenders, ask:

How many Dream For All applications have you processed?

What's your typical timeline from application to CalHFA submission?

Do you have a dedicated CalHFA specialist or team?

How will you communicate with me during the registration window?

A lender who has processed dozens of Dream For All applications will anticipate documentation requirements and potential issues. One processing their first may encounter learning-curve delays at the worst possible moment.

The Voucher Process

If selected through the lottery, applicants typically receive a reservation or voucher indicating CalHFA has allocated funding for their loan. [5] This voucher has an expiration timeline—you must find a property, get under contract, and close within the specified period.

Understanding the voucher timeline before the lottery helps you prepare your home search strategy. If you receive a voucher, you'll need to move efficiently through the purchase process while the clock runs.

Common Preparation Mistakes

After multiple funding rounds, clear patterns emerge in what derails otherwise qualified applicants.

Waiting for the Portal to Open

The biggest mistake is treating the portal opening as the start of your preparation. By the time the window opens, you should have:

Full lender pre-approval in hand

All documentation verified and current

Your lender ready to submit on your behalf

Starting from scratch when the portal opens means you're assembling documents while others are submitting complete applications.

Overlooking the First-Generation Requirement

Many applicants focus entirely on the first-time buyer definition and miss the first-generation requirement entirely. Confirming both criteria early prevents wasted effort on an application that will be automatically disqualified.

Incomplete Bank Statements

Lenders require all pages of bank statements, including blank pages that say "This page intentionally left blank." Missing pages—even seemingly unimportant ones—trigger verification delays.

Download complete statements directly from your bank's website rather than relying on mailed copies that may omit pages.

Large Deposits Without Documentation

Any deposit outside your normal pay pattern requires a paper trail. If you received a gift, sold a vehicle, or deposited cash savings, you'll need documentation explaining the source.

Undocumented large deposits can disqualify applications or delay processing past critical deadlines.

Last-Minute Co-Borrower Changes

Adding or removing a co-borrower requires restarting much of the underwriting process. If you're applying with a partner, spouse, or family member, make that decision early and complete pre-approval with all parties included from the start.

Frequently Asked Questions

What does "shared appreciation" mean, and how much will I actually owe?

Shared appreciation means CalHFA participates in your home's value increase over time. When you sell, refinance, or transfer the property, you repay the original loan amount plus a percentage of the home's appreciation since purchase. The exact percentage varies based on your income bracket when you received the loan—typically ranging from 15% to 20% of the appreciation gain. Your lender provides exact terms during application. [2]

How does the randomized drawing differ from first-come-first-served?

Previous Dream For All rounds used first-come-first-served registration, where applicants who submitted fastest received funding. The randomized drawing system assigns lottery positions randomly after the registration window closes, giving all complete applications equal odds regardless of submission timing within the window. [5]

Can I start the process without a specific home in mind?

Yes—and you should. Dream For All pre-approval and lottery registration happen before you're under contract on a property. If selected, you'll receive a voucher with a timeframe to find and close on an eligible home. Beginning lender preparation now positions you for the lottery regardless of whether you've identified a specific property.

What's the difference between "first-time" and "first-generation" homebuyer?

First-time homebuyer means you haven't owned and occupied a home as your primary residence in the past three years. First-generation homebuyer means your parents don't currently own a home in the U.S., or you were in foster care before age 18. Dream For All requires you to meet both criteria—at least one borrower must be first-generation, and all borrowers must be first-time buyers. [3]

What happens if I'm not selected in the lottery?

Unselected applicants may remain in the queue for future funding allocations if additional funds become available during the same round. For subsequent funding rounds, you'll need to reapply through the new registration process, though much of your documentation preparation will carry forward.

Your Next Step

Dream For All preparation takes time—the 30-day timeline exists because lender pre-approval, document verification, and issue resolution can't be rushed without risking disqualification.

If you're considering Dream For All as part of your homebuying strategy in the Sacramento area, mapping the program to your specific pre-approval path clarifies what you need to do and when.

Ready to build your preparation plan? Request a consult to discuss how Dream For All fits your timeline, budget, and homeownership goals.

About This Guide

This article was prepared based on publicly available CalHFA program guidelines, historical funding round procedures, and standard first mortgage preparation requirements. Tavon Willis is a California-licensed real estate salesperson (DRE #02095751) with LPT Realty, Inc., serving first-time homebuyers and relocating professionals in the Greater Sacramento area. Program details, income limits, and procedures may change between publication and the next funding round—always verify current requirements directly with CalHFA and your participating lender.

Cited Works

[1] California Housing Finance Agency — "Dream For All Program Overview." https://www.calhfa.ca.gov/dream/

[2] California Housing Finance Agency — "Shared Appreciation Loan Terms." https://www.calhfa.ca.gov/homeownership/programs/

[3] California Housing Finance Agency — "Borrower Eligibility Requirements." https://www.calhfa.ca.gov/homebuyer/programs/eligibility.htm

[4] California Housing Finance Agency — "Approved Lender List." https://www.calhfa.ca.gov/homebuyer/lenders/

[5] California Housing Finance Agency — "Dream For All Bulletins and Updates." https://www.calhfa.ca.gov/dream/updates/