Your loan type shapes how sellers see your offer. In competitive California markets like Sacramento and the Bay Area, that perception often determines whether you get the home—or lose it to another buyer.

Sellers evaluate risk. They want confidence that your deal will close on schedule without surprises. The financing you bring directly influences their assessment of that risk.

Key takeaways before we dive in:

Conventional loans typically close fastest and carry the fewest property condition hurdles

FHA loans offer easier qualification but trigger stricter appraisal requirements that can derail transactions

CalHFA down-payment assistance reduces your cash burden but extends timelines and adds underwriting layers

Pairing CalHFA with a conventional first mortgage (instead of FHA) can improve how sellers perceive your offer

Market conditions matter: these differences hit harder in seller's markets than buyer's markets

The Three Loan Types: What Each Actually Involves

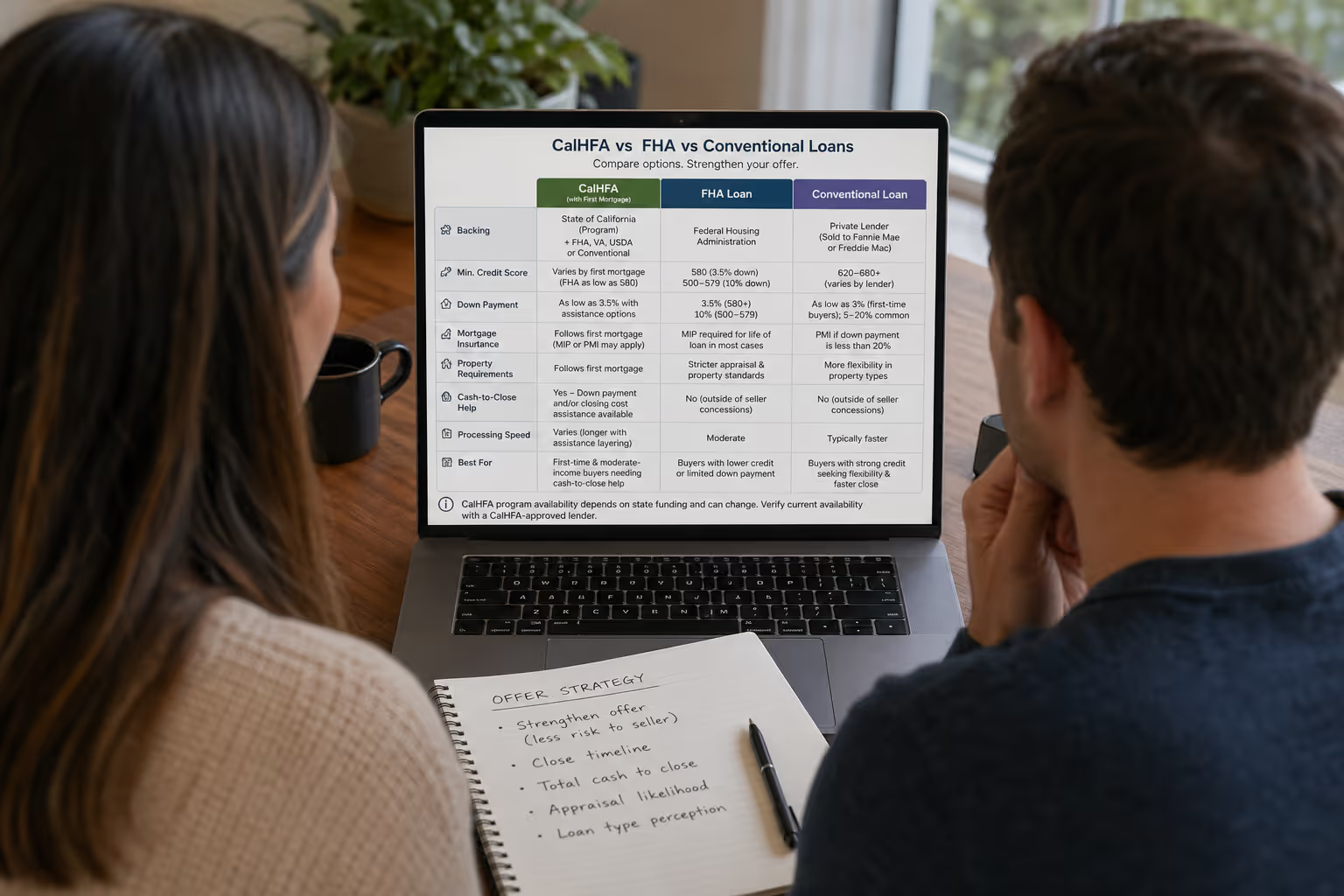

Conventional Loans

Conventional loans aren't backed by a government agency. Private lenders originate them, then typically sell them to Fannie Mae or Freddie Mac [1]. Requirements generally include:

Minimum credit scores around 620–680 (varies by lender)

Down payments as low as 3% for first-time buyers, though 5–20% is common

Private mortgage insurance (PMI) if you put down less than 20%

These loans offer the most flexibility in property types and typically process faster than government-backed options.

FHA Loans

FHA loans are insured by the Federal Housing Administration, allowing lenders to accept borrowers who might not qualify for conventional financing [2]. Key features:

Minimum credit scores as low as 580 with 3.5% down

Credit scores between 500–579 may qualify with 10% down

Mortgage insurance premiums (MIP) required for the life of the loan in most cases

Stricter property condition requirements during appraisal

CalHFA Down-Payment Assistance Programs

The California Housing Finance Agency (CalHFA) offers programs helping first-time and moderate-income buyers cover down payments and closing costs [3]. These layer on top of an underlying first mortgage—FHA, VA, USDA, or conventional—and include:

MyHome Assistance Program: A deferred-payment junior loan up to 3.5% of the purchase price

Forgivable Equity Builder Loan: Up to 10% of the purchase price, forgivable after five years for qualifying buyers

CalHFA ZIP (Zero Interest Program): Covers closing costs with a zero-interest loan

Note: CalHFA program availability depends on state funding allocations, which can be depleted and replenished throughout the year. Always verify current availability with a CalHFA-approved lender before building your offer strategy around specific programs.

These programs significantly reduce cash-to-close requirements—but they create trade-offs that affect how sellers perceive your offer.

How Sellers Evaluate Financing: The Risk Calculation

When a listing agent reviews multiple offers, they're running a mental risk assessment:

Will this buyer actually close?

How likely is the appraisal to create problems?

How long will this take?

What could derail the transaction?

Your loan type directly shapes every answer.

Cash-to-Close Certainty

Conventional loans signal the strongest cash position. A buyer putting 10–20% down demonstrates significant reserves. Even at 3–5% down, conventional buyers typically have more flexibility to cover appraisal gaps or unexpected costs.

FHA loans require only 3.5% down, which can signal thinner reserves. Sellers sometimes worry an FHA buyer won't have funds available if issues emerge during escrow.

CalHFA-assisted offers present a nuanced picture. Layered financing—a first mortgage plus one or two subordinate assistance loans—creates more moving parts. If any program hits a snag, the entire transaction can stall [4].

That said, CalHFA assistance means the buyer isn't draining personal savings to close. Experienced listing agents recognize this distinction.

Appraisal Risk: Where Loan Type Creates Real Differences

Conventional appraisals follow standard guidelines focused primarily on market value. If the appraisal comes in low, buyer and seller can negotiate—or the buyer can cover the gap with cash.

FHA appraisals carry stricter property condition requirements. The appraiser must confirm the home meets HUD's minimum property standards for safety, security, and structural soundness [5]. Common issues that derail FHA transactions:

Peeling paint (especially in pre-1978 homes due to lead paint concerns)

Missing handrails on stairs

Broken windows

Non-functional HVAC, plumbing, or electrical systems

If the appraiser flags these issues, repairs must be completed before closing—or the deal falls apart. I frequently see sellers choose a conventional offer over an FHA offer at the same price simply because they don't want the appraisal headache.

CalHFA appraisals follow the requirements of the underlying loan type. A CalHFA loan paired with an FHA first mortgage carries FHA property standards. Paired with a conventional first mortgage, it follows less restrictive conventional guidelines.

Strategic insight: If you're using CalHFA assistance and you qualify for conventional financing, pairing your assistance with a conventional first mortgage can improve your offer's appeal by avoiding FHA property requirements entirely.

Escrow Timeline: Speed Matters in Competitive Markets

Sellers often prefer shorter escrows. A 30-day close is standard for conventional financing in many California markets; some conventional transactions close even faster.

FHA loans typically require 30–45 days due to additional documentation requirements and the FHA appraisal process [6].

CalHFA-assisted transactions often need 45–60 days because down-payment assistance involves additional underwriting layers, compliance checks, and coordination between multiple loan programs [4]. Some CalHFA-approved lenders have streamlined their processes, but extended timelines remain common.

In a hot seller's market—which describes much of Sacramento and the broader California market in recent years—a longer escrow can cost you the home. When you're competing against conventional or cash offers, timeline becomes a significant disadvantage.

In a buyer's market, these differences matter less. Sellers with homes sitting longer become more flexible about escrow length and financing complexity.

Debt-to-Income Ratio: A Hidden Factor

Your debt-to-income (DTI) ratio measures monthly debt payments against gross monthly income. While primarily a qualification metric, it indirectly affects offer strength.

Conventional loans typically allow DTI ratios up to 43–45%, with flexibility up to 50% for strong applications [7].

FHA loans may permit higher DTI ratios (up to 50% or slightly beyond with compensating factors), helping more buyers qualify [2].

CalHFA programs have their own DTI limits that may be more restrictive than the underlying loan program, depending on which CalHFA product you're using [3].

Why does this matter for offer strength? Buyers with lower DTI ratios have more financial cushion. If rates shift slightly before closing or unexpected costs emerge, they're less likely to fall out of escrow. Some listing agents factor this in when advising sellers on offer selection.

Seller Credits: A Strategic Consideration

Requesting seller credits (also called seller concessions) to cover closing costs affects your offer's attractiveness.

Conventional loans allow seller credits up to:

3% of the purchase price if you put down less than 10%

6% if you put down 10–25%

9% if you put down more than 25% [8]

FHA loans allow seller credits up to 6% of the purchase price [2].

CalHFA-assisted buyers should be strategic about stacking assistance. If you're already receiving down-payment help through CalHFA, requesting substantial seller credits on top may signal thin financial reserves—potentially weakening your offer in competitive situations.

Practical approach: If you're using CalHFA assistance, consider limiting your seller credit request to cover only essential costs. This demonstrates you're not stretching beyond your means while still managing your cash-to-close.

Timeline Comparison by Loan Type

| Loan Type | Typical Escrow Period | Common Delays |

| Conventional | 25–35 days | Appraisal scheduling, document requests |

| FHA | 30–45 days | Property condition issues, FHA appraisal backlog |

| CalHFA + Conventional | 40–55 days | Subordinate loan processing, compliance review |

| CalHFA + FHA | 45–60+ days | Combined FHA requirements + CalHFA processing |

Timelines vary by lender, market conditions, and transaction complexity.

Three Buyer Scenarios: How Sellers See Your Offer

Consider how different financing looks to a seller evaluating offers on a $500,000 home in the Sacramento area.

Buyer A: Conventional (10% Down)

Down payment: $50,000

Cash-to-close certainty: High—significant reserves demonstrated

Appraisal risk: Standard property requirements

Timeline: 30 days

Seller perception: Strong, straightforward transaction likely

Buyer B: FHA (3.5% Down)

Down payment: $17,500

Cash-to-close certainty: Moderate—limited reserves possible

Appraisal risk: FHA property standards apply; older homes face more scrutiny

Timeline: 35–40 days

Seller perception: Acceptable, but property condition may create issues

Buyer C: CalHFA + Conventional (3% down + 3% assistance)

Down payment: $15,000 (assisted)

Cash-to-close certainty: Lower—layered financing creates complexity

Appraisal risk: Standard conventional requirements (avoiding FHA hurdles)

Timeline: 45–50 days

Seller perception: More moving parts and longer timeline, but avoids worst appraisal risks

CalHFA-assisted buyers can absolutely win offers. The key is understanding these dynamics and structuring your approach strategically.

How Market Conditions Change the Equation

The impact of your financing choice depends heavily on whether you're buying in a seller's market or buyer's market.

In a seller's market (low inventory, multiple offers common):

Timeline differences hit hard—a 45-day escrow competes poorly against 30 days

Appraisal concerns loom larger because sellers have alternatives

Financing complexity becomes a meaningful disadvantage

You'll need to strengthen other offer terms to compensate

In a buyer's market (more inventory, fewer competing offers):

Sellers become more flexible on timeline

Financing type matters less when offers are scarce

CalHFA and FHA buyers face less competitive pressure

Sellers may accept longer escrows rather than wait for another offer

Sacramento's market conditions have shifted over recent years, and they vary by neighborhood and price point. Understanding current conditions in your target areas helps you calibrate how much your financing choice will affect competitiveness.

Strengthening a CalHFA-Assisted Offer

If you're using down-payment assistance, these strategies improve your competitiveness:

Choose the right underlying loan: When you qualify for both, pair CalHFA assistance with a conventional first mortgage instead of FHA. You'll avoid stricter property requirements and signal a cleaner transaction.

Get fully underwritten before you make offers: Some lenders offer "TBD underwriting" or "loan commitment letters" that demonstrate your financing is solid—not just pre-approved, but actually reviewed and cleared pending only the property. This carries significantly more weight with listing agents [9].

Target properties strategically: Focus your search on homes less likely to trigger appraisal issues. Well-maintained properties reduce everyone's risk. Newer construction often presents fewer condition concerns.

Strengthen other terms: A slightly higher earnest money deposit, shorter inspection contingency period, or flexible closing date can offset concerns about financing complexity. These adjustments show commitment and reduce seller uncertainty.

Work with experienced professionals: A lender who processes CalHFA transactions regularly can often close faster than one handling these loans occasionally. Ask specifically about their CalHFA volume and average close times.

Write a clean offer: Minimize unusual contingencies or requests. The simpler your offer appears, the less risk sellers perceive.

What This Means for Your Strategy

Understanding how financing affects offer strength isn't about discouraging you from using helpful programs. CalHFA down-payment assistance exists because it helps California buyers who wouldn't otherwise have enough saved for a down payment. These programs have helped thousands of families achieve homeownership [3].

Knowledge is leverage. When you understand how sellers evaluate offers, you can:

Structure your offer to address common concerns before they become objections

Target homes where your financing creates the least friction

Set realistic expectations about competition in your price range

Work with professionals who know how to position assistance-backed offers effectively

The "right" loan program depends on your complete financial picture, your timeline, and current market conditions where you're buying. A comparison chart only tells part of the story.

Next Steps: Building Your Financing Strategy

If you're considering CalHFA assistance or deciding between FHA and conventional financing, the best next step is a detailed conversation with a lender who understands California-specific programs—and can explain how each option affects your competitiveness in your target neighborhoods.

Want help building a financing strategy that strengthens your offer? Request a financing strategy call with our preferred lender network. We'll connect you with professionals who specialize in California first-time buyer programs and can show you exactly how your options translate into offer strength.

Frequently Asked Questions

Does using CalHFA down-payment assistance hurt my chances of getting an offer accepted?

It changes how sellers perceive your offer, but it doesn't automatically hurt your chances. CalHFA assistance extends escrow timelines and adds financing layers, which some sellers view as higher risk. You can offset these concerns by pairing assistance with a conventional first mortgage, getting fully underwritten before making offers, and working with lenders experienced in CalHFA transactions. In buyer's markets, these differences matter less.

Which loan type closes fastest in California?

Conventional loans typically close fastest, often in 25–35 days. FHA loans generally require 30–45 days due to additional documentation and property condition reviews. CalHFA-assisted transactions frequently need 45–60 days because of additional underwriting layers and compliance requirements across multiple loan programs.

Can I use CalHFA assistance with a conventional loan instead of FHA?

Yes. CalHFA offers programs compatible with conventional first mortgages, not just FHA loans. This pairing avoids FHA's stricter property condition requirements during appraisal, which may make your offer more appealing to sellers concerned about inspection and appraisal complications—particularly on older homes.

Why do some sellers prefer conventional loans over FHA?

FHA appraisals require the property to meet HUD's minimum property standards, which means the appraiser checks for safety and condition issues beyond just market value. Problems like peeling paint, missing handrails, or deferred maintenance can require repairs before closing. Sellers often prefer conventional offers because the appraisal process is simpler and less likely to create last-minute complications.

Should I request seller credits if I'm using down-payment assistance?

Be strategic. Stacking CalHFA assistance with large seller credit requests may signal thin financial reserves, potentially weakening your offer in competitive situations. If you're using down-payment help, consider limiting seller credits to essential costs only. This demonstrates your financing package is solid while still managing your out-of-pocket expenses.

About This Content

This article provides educational guidance on California home financing options. The information draws from publicly available program guidelines, industry standards, and regulatory sources. Tavon Willis is a California-licensed real estate salesperson (DRE #02095751) serving the Greater Sacramento area, including Elk Grove and surrounding communities. This content is intended for general educational purposes and does not constitute financial or legal advice. Program terms, requirements, and availability change—always verify current details with qualified lending professionals.

Cited Works

[1] Consumer Financial Protection Bureau — "What is a conventional loan?" https://www.consumerfinance.gov/ask-cfpb/what-is-a-conventional-loan-en-100/

[2] U.S. Department of Housing and Urban Development — "Let FHA Loans Help You." https://www.hud.gov/buying/loans

[3] California Housing Finance Agency — "Homebuyer Programs." https://www.calhfa.ca.gov/homebuyer/programs/

[4] California Housing Finance Agency — "CalHFA Lender Resources." https://www.calhfa.ca.gov/homebuyer/lenders/

[5] U.S. Department of Housing and Urban Development — "Minimum Property Requirements." https://www.hud.gov/program_offices/housing/sfh/handbook_702

[6] Consumer Financial Protection Bureau — "How long does it take to close on a house?" https://www.consumerfinance.gov/ask-cfpb/how-long-does-it-take-to-close-on-a-house-en-2005/

[7] Fannie Mae — "Selling Guide: Debt-to-Income Ratios." https://selling-guide.fanniemae.com/

[8] Fannie Mae — "Selling Guide: Interested Party Contributions." https://selling-guide.fanniemae.com/

[9] Consumer Financial Protection Bureau — "What is a loan estimate?" https://www.consumerfinance.gov/ask-cfpb/what-is-a-loan-estimate-en-1995/