Quick rule of thumb: Plan for 5% to 10% of the purchase price in total cash beyond your down payment—though your exact number depends on loan type, negotiations, and how much cushion you want after closing.

I've watched buyers in Elk Grove and across Sacramento get pre-approved, find a home they love, and then hit a wall three weeks before closing: their cash-to-close number was thousands higher than expected. The down payment they'd saved for? That was only one piece of the puzzle.

Most first-time buyers dramatically underestimate their total cash requirements because they focus on a single number when they actually need to plan for five separate buckets. Understanding each bucket—and knowing exactly where to find those line items on your Loan Estimate—can mean the difference between a smooth closing and a scramble to find funds at the last minute.

Here's what your cash picture actually looks like when you buy a home in Sacramento.

The Five Cash Buckets Every Sacramento Buyer Must Plan For

When you buy a home, your cash requirements fall into five distinct categories. Each serves a different purpose, hits your bank account at a different time, and appears on different lines of your Loan Estimate.

The framework:

Down payment – Your equity stake in the property

Closing costs – Fees to complete the transaction

Prepaids – Expenses paid in advance at closing

Reserves – Cash you keep after closing

Moving and settling-in costs – Often forgotten, always necessary

A Sacramento home priced at $500,000 might require anywhere from $25,000 to $125,000 in total cash depending on your loan program, negotiating power, and how much cushion you want.

Bucket 1: Your Down Payment

The down payment is the portion of the purchase price you pay upfront in cash. It becomes your immediate equity in the home.

Down Payment Ranges by Loan Type

Different loan programs have different minimum requirements [1]:

| Loan Type | Minimum Down Payment | On a $500,000 Home |

| Conventional | 3% (first-time buyers) to 5% | $15,000–$25,000 |

| FHA | 3.5% | $17,500 |

| VA | 0% | $0 |

| USDA | 0% | $0 |

| Jumbo | Typically 10–20% | $50,000–$100,000 |

For conventional loans, putting down less than 20% means you'll pay private mortgage insurance (PMI), which adds to your monthly payment until you reach sufficient equity [2].

What This Looks Like in Sacramento

The Sacramento-Roseville-Folsom metropolitan area had a median home price of approximately $540,000 as of early 2025, according to California Association of Realtors data [3]. At that price point:

3% down = roughly $16,200

10% down = roughly $54,000

20% down = roughly $108,000

Your down payment appears on Page 1 of your Loan Estimate under "Loan Terms" as a component of the calculation, and on Page 2 in the "Calculating Cash to Close" section [4].

Bucket 2: Closing Costs

Closing costs cover the services required to originate your loan and transfer ownership. These fees go to lenders, title companies, appraisers, and government entities.

Typical Closing Cost Components

Closing costs in California generally range from 2% to 5% of the purchase price, though this varies based on your lender, loan type, and specific transaction [5]. On a $500,000 Sacramento home, expect roughly $10,000 to $25,000.

Key takeaway: Closing costs are separate from your down payment and catch many buyers off guard.

Here's where that money goes:

Lender Fees (Section A on Loan Estimate)

Origination charges

Underwriting fees

Processing fees

Points (if buying down your rate)

Third-Party Services (Sections B and C on Loan Estimate)

Appraisal fee: typically $400–$700 in the Sacramento area

Credit report fee

Title insurance (both lender's and owner's policies)

Escrow/settlement fees

Notary fees

Government Fees (Section E on Loan Estimate)

Recording fees

Transfer taxes (in Sacramento County, this is typically calculated per $1,000 of sale price) [6]

Where to Find These on Your Loan Estimate

Your Loan Estimate breaks down closing costs on Page 2 under "Loan Costs" and "Other Costs." The form organizes fees into lettered sections (A through H) that show exactly what you're paying and to whom [4].

Pro tip: Compare Loan Estimates from multiple lenders by looking at Section A (origination charges). This is where lenders have the most flexibility to compete on price.

Bucket 3: Prepaids

Prepaids are expenses you pay at closing to cover costs that technically come due after you own the home. Think of them as advance payments that fund your escrow account and cover your initial insurance premium.

What Gets Prepaid

Homeowner's Insurance Premium

Most lenders require you to pay your first full year of homeowner's insurance at closing. In California, homeowner's insurance costs vary widely based on location, home age, and coverage level. Sacramento-area homeowners typically pay between $1,200 and $3,000 annually, though costs have increased in recent years due to wildfire risk factors across California [7].

Property Tax Escrow

Your lender collects several months of property taxes upfront to establish your escrow account. California property tax rates are approximately 1% of assessed value (Proposition 13), plus local assessments that vary by county and special district [8].

Important for Sacramento suburbs: If you're buying in Elk Grove, Folsom, Roseville, Natomas, or other newer developments, ask about Mello-Roos taxes. These special assessment districts fund infrastructure and services in master-planned communities, and they can add significantly to your property tax bill—sometimes hundreds of dollars per month. Mello-Roos assessments directly impact how much your lender collects for escrow at closing, which increases your prepaids.

Prepaid Interest

You'll pay interest from your closing date through the end of that month. Close on the 1st and you pay nearly a full month; close on the 28th and you pay just a few days.

Where to Find These on Your Loan Estimate

Prepaids appear on Page 2 in Section F ("Prepaids") and Section G ("Initial Escrow Payment at Closing"). These line items confuse many buyers because they can add $3,000 to $8,000+ to your cash requirement [4].

Bucket 4: Reserves

Here's a bucket that doesn't appear on your Loan Estimate at all—but your lender absolutely cares about it.

Reserves are funds you have left over after paying your down payment, closing costs, and prepaids. They prove you can survive financially if something unexpected happens in your first months of ownership.

Reserve Requirements by Loan Type

Different loans have different reserve requirements:

Conventional loans: Often require 2–6 months of mortgage payments in reserves, depending on credit score, down payment, and property type [9]

FHA loans: Generally no reserve requirement for primary residences

VA loans: Generally no reserve requirement for primary residences

Jumbo loans: Typically require 6–12+ months of reserves

For a $500,000 Sacramento home with a $3,500 monthly payment (including taxes and insurance), two months of reserves equals $7,000. Six months equals $21,000.

Important: Reserve requirements vary by lender and borrower profile. Your loan officer can tell you exactly what's required for your situation.

Why Reserves Matter Beyond Requirements

Even if your loan program requires minimal reserves, maintaining a cushion makes sense. Owning a home brings surprises: a water heater fails, an HVAC system needs repair, or property taxes increase. Financial experts often suggest having 3–6 months of living expenses accessible after you move in [10].

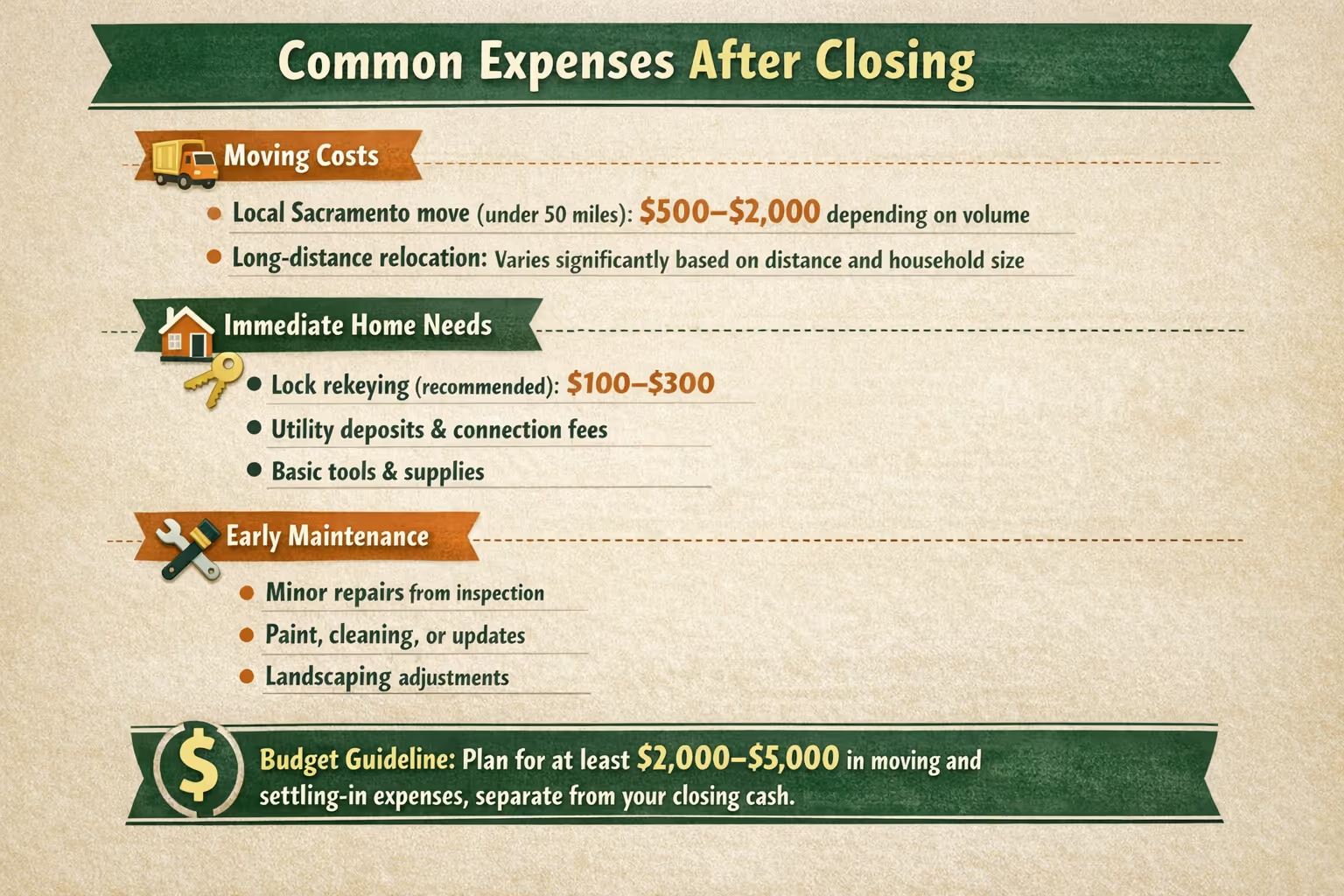

Bucket 5: Moving and Settling-In Costs

This is the bucket buyers most often forget when calculating their cash needs—and it hits right when cash feels tightest.

Common Expenses After Closing

Moving Costs

Local Sacramento move (under 50 miles): $500–$2,000 depending on volume

Long-distance relocation: varies significantly based on distance and household size

Immediate Home Needs

Lock rekeying (recommended): $100–$300

Utility deposits and connection fees

Basic tools and supplies

Early Maintenance

Many buyers discover needs shortly after moving in:

Minor repairs the inspection noted but weren't addressed

Paint, cleaning, or cosmetic updates

Landscaping adjustments (especially relevant in Sacramento's climate)

Budget guideline: Plan for at least $2,000–$5,000 in moving and settling-in expenses, separate from your closing cash.

California Down Payment Assistance Programs

If the cash requirements above feel daunting, you're not alone—and there are programs designed to help.

The California Housing Finance Agency (CalHFA) offers several down payment assistance programs for first-time buyers and repeat buyers who meet income and purchase price limits.

Common CalHFA programs include:

MyHome Assistance Program: A deferred-payment junior loan up to a percentage of the purchase price for down payment and closing costs

Zero Interest Program (ZIP): A zero-interest loan that can help bridge cash gaps

Eligibility depends on income limits (which vary by county), homebuyer education requirements, and using a CalHFA-approved lender. Sacramento County has specific income limits that change annually.

What to do: Ask your lender early whether you qualify for any down payment assistance. These programs have specific requirements and timelines, so knowing your options before you're under contract gives you more flexibility.

How to Read Your Loan Estimate Line by Line

The Loan Estimate is a standardized three-page document that every lender must provide within three business days of receiving your mortgage application [4]. In my experience helping buyers in Sacramento and Elk Grove, this is the document that answers most cash-to-close questions—if you know where to look.

Page 1: Loan Terms and Costs Summary

Loan Amount: What you're borrowing (purchase price minus down payment)

Interest Rate: Your locked or estimated rate

Monthly Principal & Interest: Core housing payment

Estimated Total Monthly Payment: Includes taxes, insurance, and PMI if applicable

Page 2: Closing Cost Details

This is where you see your cash picture:

Section A: Origination Charges

These are lender fees. If you see a large number here, compare it to other lenders' quotes.

Section B: Services You Cannot Shop For

Appraisal, credit report, flood determination—required services chosen by your lender.

Section C: Services You Can Shop For

Title services, settlement services, survey (if required). You can often select your own providers here.

Section E: Taxes and Government Fees

Recording fees, transfer taxes—set by local government.

Section F: Prepaids

Homeowner's insurance premium, mortgage interest, property taxes prepaid at closing.

Section G: Initial Escrow Payment

Months of taxes and insurance collected to start your escrow account.

Page 3: Comparisons and Contact Information

Shows how your loan compares over time and provides contact information for your lender, mortgage broker (if applicable), and settlement agent.

The "Calculating Cash to Close" Table

At the bottom of Page 2, you'll find a summary table that shows:

Total closing costs

Minus any credits (including seller credits and lender credits)

Plus or minus adjustments

Equals your Cash to Close estimate

This number plus your reserves plus your moving budget equals your true cash requirement.

Seller Credits: How to Reduce Your Cash Requirement

One of the most effective ways to lower your upfront cash is negotiating seller credits (also called seller concessions).

How Seller Credits Work

The seller agrees to pay a portion of your closing costs. This comes out of their proceeds rather than your pocket. The credit appears on your Loan Estimate in the "Calculating Cash to Close" section and reduces your cash requirement dollar-for-dollar [12].

Seller Credit Limits by Loan Type

Loan programs cap how much sellers can contribute:

| Loan Type | Down Payment | Maximum Seller Credit |

| Conventional | Less than 10% | 3% of purchase price |

| Conventional | 10–25% | 6% of purchase price |

| Conventional | 25%+ | 9% of purchase price |

| FHA | Any | 6% of purchase price |

| VA | Any | 4% of purchase price |

On a $500,000 home with 5% down, a seller could contribute up to $15,000 (3%) toward your closing costs [12].

When Sellers Are Most Likely to Agree

Seller credits are negotiation items. Your leverage depends on:

Market conditions (buyer's market vs. seller's market)

Days on market for the property

Competing offers

How motivated the seller is

Your real estate agent can advise on what's realistic in current Sacramento market conditions.

Earnest Money Deposit: Your Good-Faith Cash

When you make an offer on a Sacramento home, you'll typically submit an earnest money deposit (EMD) to show you're serious. This isn't an additional cost—it's an advance on your down payment.

Typical Earnest Money Amounts

In the Sacramento area, earnest money deposits commonly range from 1% to 3% of the purchase price, though amounts vary by neighborhood and market conditions. On a $500,000 home, expect $5,000 to $15,000.

What Happens to Your Earnest Money

If the deal closes: Your EMD is credited toward your down payment and closing costs

If you cancel within contingency periods: You typically get your EMD back (subject to contract terms)

If you cancel outside contingency protections: You may lose some or all of your EMD

Your earnest money needs to be liquid and accessible quickly after your offer is accepted—usually within 1–3 business days.

A Sacramento Cash Requirement Example

Here's a realistic scenario based on what I see working with buyers:

Purchase price: $520,000 (close to Sacramento metro median)

Down payment: 5% conventional loan

Loan program: Conventional with PMI

| Cash Bucket | Estimated Amount |

| Down payment (5%) | $26,000 |

| Closing costs (2.5% estimate) | $13,000 |

| Prepaids (insurance + escrow setup) | $5,000 |

| Reserves (2 months required) | $7,000 |

| Moving/settling-in budget | $3,000 |

| Total Cash Needed | $54,000 |

Now assume you negotiate $10,000 in seller credits:

| Adjusted Cash Requirement | |

| Cash to close (reduced by seller credit) | $34,000 |

| Reserves | $7,000 |

| Moving budget | $3,000 |

| Adjusted Total | $44,000 |

That negotiation saved you $10,000 in immediate cash—while the seller credit reduces what comes out of your pocket at closing.

Common Mistakes That Create Cash Crunches

Mistake 1: Ignoring the Loan Estimate Until Closing Week

Your Loan Estimate gives you critical cash-to-close information early. Review it within days of receiving it, not weeks later. If the numbers don't work, you need time to adjust.

Mistake 2: Confusing Loan Estimate Numbers with Final Numbers

The Loan Estimate is an estimate. Your Closing Disclosure—provided at least three business days before closing—shows final numbers [4]. Expect some variation between the two documents.

Mistake 3: Draining Every Account to Close

Lenders verify your assets close to closing. If your reserves dip below requirements, your loan can be delayed or denied. Maintain the cash cushion your lender requires throughout the process.

Mistake 4: Forgetting Earnest Money Timing

Your earnest money deposit often comes due within days of offer acceptance. If those funds are locked in CDs or investment accounts, you may face delays or penalties.

Mistake 5: Overlooking Mello-Roos in New Communities

Buying in a newer Sacramento-area development? Mello-Roos assessments can significantly increase your property tax escrow requirements. Ask specifically about special assessments before making an offer.

How to Prepare Your Cash Position

Step 1: Get Pre-Approved Before Searching

Pre-approval tells you exactly what loan amount, down payment percentage, and reserve requirements apply to your situation. Without this, you're guessing.

Step 2: Request a Sample Loan Estimate Early

Ask your lender to generate a Loan Estimate based on a hypothetical purchase price similar to homes you're considering. This shows realistic closing costs before you're under contract pressure.

Step 3: Keep Cash in Accessible, Documented Accounts

Lenders want to see your funds in checking, savings, or money market accounts with clear paper trails. Large recent deposits will need explanation. Gift funds have specific documentation requirements [13].

Step 4: Build Your Reserves Now

If your loan requires three months of reserves and you need $10,000, start building that cushion months before you expect to close. Don't assume you'll find the money later.

Step 5: Budget for Post-Closing Reality

New homeownership brings expenses. Utility bills often increase. Maintenance happens. Build a post-closing cash buffer so you're not financially stressed on day one.

Get Clarity on Your Cash-to-Close Numbers

Understanding how much cash you need to buy a home in Sacramento is the foundation of a confident purchase. Once your lender provides a Loan Estimate, you can see exactly where your money goes—and identify opportunities to reduce your out-of-pocket costs through seller credits, lender credits, or down payment assistance programs.

If you've received a Loan Estimate and want help understanding the numbers—or you're planning ahead and want to know what to expect—request a cash-to-close review. We'll walk through your Loan Estimate line by line so you close with confidence.

Call us or request a consult to get started.

Frequently Asked Questions

What's the difference between down payment and closing costs?

Your down payment is the portion of the home's purchase price you pay in cash—it becomes your immediate equity in the property. Closing costs are separate fees that pay for services like appraisals, title insurance, loan origination, and government recording. Both require cash at closing, but they serve different purposes and appear in different sections of your Loan Estimate.

Can I use gift money for my down payment and closing costs in California?

Many loan programs allow gift funds from family members for down payments and sometimes closing costs. However, lenders require specific documentation, including a gift letter stating the money doesn't need to be repaid and proof of the donor's ability to give [13]. Requirements vary by loan type, so discuss this with your lender early.

What are reserves, and do I really need them to buy a home?

Reserves are funds you maintain after paying all closing costs—your financial cushion as a new homeowner. Some loan programs, particularly conventional and jumbo loans, require proof of reserves (often 2–6 months of mortgage payments) before approving your loan [9]. Even when not required, reserves protect you from unexpected home expenses in your first months of ownership.

How can I lower my cash-to-close amount?

Common strategies include negotiating seller credits (where the seller pays a portion of your closing costs), asking about lender credits (where a slightly higher interest rate funds a credit toward closing costs), exploring down payment assistance programs like CalHFA, and choosing loan programs with lower down payment requirements. Your Loan Estimate shows how credits reduce your cash-to-close figure.

When do I pay earnest money, and is it separate from my down payment?

You typically pay earnest money within a few days of your offer being accepted—it demonstrates good faith to the seller. At closing, your earnest money is credited toward your down payment and closing costs. It's not an additional expense; it's an advance on what you'll owe.

About the Author

Tavon Willis is a California-licensed real estate salesperson (DRE #02095751) serving the Greater Sacramento area, including Elk Grove and surrounding communities. He focuses on helping first-time buyers, relocating professionals, and military families navigate the homebuying process with education-first guidance and practical strategy. His approach emphasizes clarity over pressure—helping buyers understand their numbers and make confident decisions.

Cited Works

[1] Consumer Financial Protection Bureau — "Determine Your Down Payment." https://www.consumerfinance.gov/owning-a-home/prepare/determine-your-down-payment/

[2] Consumer Financial Protection Bureau — "What Is Private Mortgage Insurance?" https://www.consumerfinance.gov/ask-cfpb/what-is-private-mortgage-insurance-en-122/

[3] California Association of Realtors — "Housing Market Data." https://www.car.org/marketdata

[4] Consumer Financial Protection Bureau — "Loan Estimate Explainer." https://www.consumerfinance.gov/owning-a-home/loan-estimate/

[5] Consumer Financial Protection Bureau — "What Are Closing Costs?" https://www.consumerfinance.gov/ask-cfpb/what-are-closing-costs-en-1845/

[6] Sacramento County Assessor's Office — "Transfer Tax Information." https://assessor.saccounty.gov/

[7] California Department of Insurance — "Homeowners Insurance." https://www.insurance.ca.gov/01-consumers/105-type/95-guides/01-homeowners/

[8] California State Board of Equalization — "Proposition 13." https://www.boe.ca.gov/proptaxes/prop13.htm

[9] Fannie Mae — "Selling Guide: Asset Requirements." https://selling-guide.fanniemae.com/

[10] Consumer Financial Protection Bureau — "Emergency Savings." https://www.consumerfinance.gov/consumer-tools/save-for-emergencies/

[11] California Housing Finance Agency — "Homebuyer Programs." https://www.calhfa.ca.gov/homebuyer/programs/

[12] Fannie Mae — "Interested Party Contributions." https://selling-guide.fanniemae.com/

[13] Consumer Financial Protection Bureau — "Gift Money for a Down Payment." https://www.consumerfinance.gov/ask-cfpb/can-i-use-gifted-funds-for-a-down-payment-en-1987/