Selling your home fast sounds appealing. No showings, no staging, no waiting months for the right buyer. iBuyers and "we buy houses" companies promise exactly that—a quick, hassle-free sale.

But here's what most sellers don't realize until they're deep into the process: the contract matters more than the headline offer.

That initial number you see? It's rarely what you'll walk away with. Between service fees, repair credits, and contract clauses that shift risk onto you, the gap between the offer price and your actual net proceeds can be substantial. Understanding how to evaluate iBuyers and "we buy houses" contracts before you sign is the difference between a smart decision and an expensive mistake.

This guide breaks down the fee structures, repair credits, and contract red flags you need to know—without the jargon. By the end, you'll have a practical framework for comparing offers and protecting your interests.

What Are iBuyers and "We Buy Houses" Companies?

Before diving into contracts, let's clarify who we're talking about. These two categories operate differently, and the distinctions affect what you'll find in their paperwork.

iBuyers (Instant Buyers)

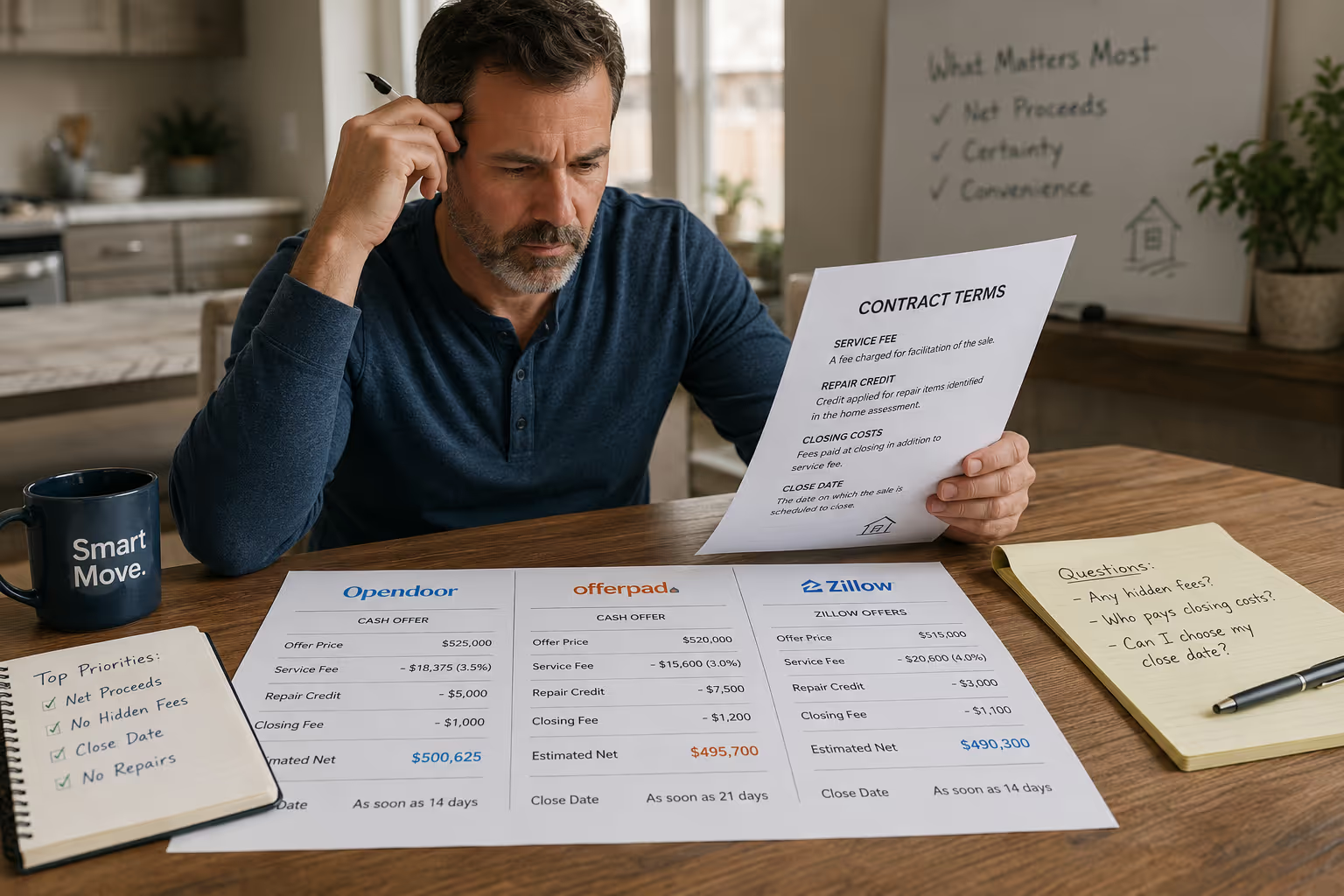

iBuyers are technology-driven companies that use algorithms to make rapid purchase offers on homes. Major players include Opendoor, Offerpad, and (historically) Zillow Offers. [1]

They typically:

Target homes in good condition within specific markets

Provide offers within 24–48 hours

Close in as few as 14 days or let you choose your timeline

Charge a service fee (often comparable to or higher than traditional real estate commissions)

"We Buy Houses" Companies

This category includes local investors, house flippers, and wholesalers who purchase properties for cash. You've likely seen their signs at intersections or received their postcards.

They typically:

Buy properties in any condition (including distressed homes)

Offer significant discounts below market value

Close extremely fast (sometimes within a week)

May use assignment clauses to flip contracts to other buyers

Both promise speed and convenience. Neither is inherently good or bad—but both require you to read the fine print carefully.

Understanding Fee Structures: What Actually Gets Deducted

The offer price on a cash-buyer contract is a starting point, not a finish line. Here's what typically comes off the top.

Service Fees

iBuyers charge service fees that function similarly to real estate commissions—but they're often higher.

According to a Bankrate analysis, iBuyer service fees typically range from 5% to 6% of the sale price, though some companies have charged up to 13–15% in certain markets. [2] For context, traditional real estate commissions have historically averaged around 5–6% total (split between buyer and seller agents), though this varies and has been evolving.

What to check: Look for the exact percentage in your contract. Some companies advertise low service fees but build costs into other line items.

Repair Credits

This is where many sellers experience sticker shock.

Most iBuyers conduct an inspection after you accept their initial offer. Based on that inspection, they'll request a "repair credit"—a deduction from your sale price to cover the cost of repairs they'll handle after closing.

Here's the catch: you often have no say in the repair estimates, no ability to get competing bids, and limited options to dispute the amounts. A Marketwatch analysis found that repair credits can range from a few thousand dollars to tens of thousands, depending on the home's condition. [3]

What to check:

Is the repair credit capped at a certain amount?

Can you dispute the repair estimate or get your own inspection?

What happens if the repair credit exceeds what you're comfortable with—can you walk away without penalty?

Closing Costs

Like any real estate transaction, you'll typically pay closing costs. These might include title insurance, escrow fees, transfer taxes, and other standard charges.

Some iBuyers roll these into their service fee; others list them separately. Either way, you need to see the complete picture.

What to check: Ask for a net proceeds estimate that accounts for all deductions—service fee, repair credits, and closing costs. Compare this number (not the offer price) to what you'd likely net from a traditional sale.

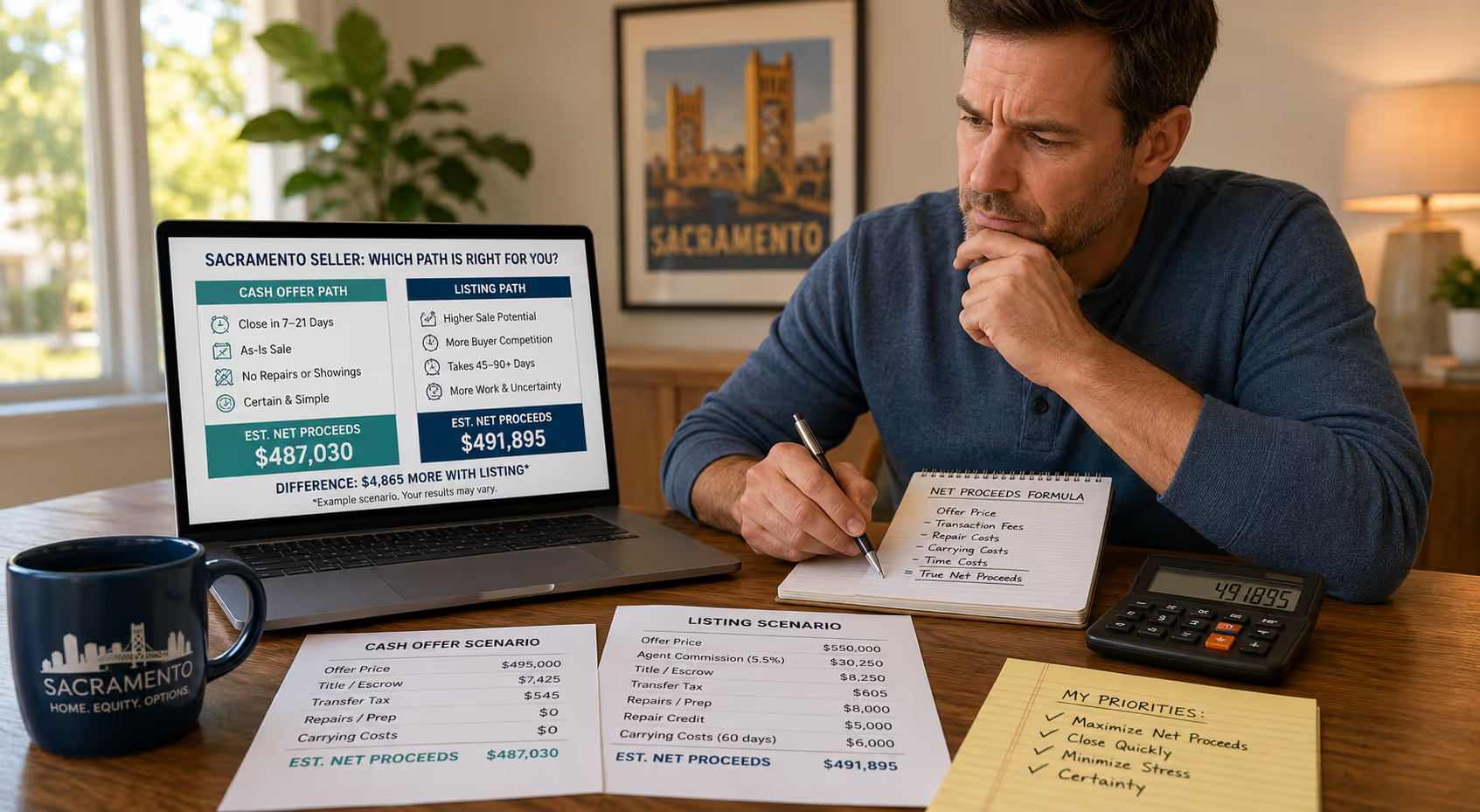

The Net Proceeds Comparison

Here's a simplified example:

| Factor | iBuyer Sale | Traditional Sale |

| Offer/Sale Price | $400,000 | $420,000 |

| Service Fee/Commission | $24,000 (6%) | $21,000 (5%) |

| Repair Credit | $15,000 | $5,000 (negotiated) |

| Closing Costs | $4,000 | $4,000 |

| Net Proceeds | $357,000 | $390,000 |

In this scenario, the convenience of the iBuyer sale comes at a $33,000 cost. That might be worth it to some sellers—but only if you know the tradeoff upfront.

Common Contract Clauses Explained in Plain English

Cash-buyer contracts often contain clauses you won't find in standard purchase agreements. Here's what to look for and what they actually mean.

The Assignment Clause

What it says: "Buyer may assign this contract to another party without seller's consent."

What it means: The company can sell your contract to someone else before closing. They're not actually buying your home—they're securing the right to buy it, then flipping that right to another investor for a profit.

Why it matters: You might think you're selling to Company A, but Company B actually shows up at closing. The original company pockets the difference between what they offered you and what they sold the contract for.

Red flag level: Not inherently problematic, but you deserve to know who's actually buying your property. Some sellers specifically want to avoid this.

Inspection Contingency (One-Sided)

What it says: "Buyer may conduct inspections and, at Buyer's sole discretion, terminate this agreement or renegotiate the purchase price."

What it means: They can back out or demand a price reduction based on their inspection—but you're often locked in once you sign.

Why it matters: This creates an imbalance. They can walk away easily; you might face penalties for doing the same.

Red flag level: High, especially if there's no cap on how much they can reduce the price or no clear exit for you.

The "As-Is" Clause

What it says: "Property is sold in as-is condition. Seller makes no warranties regarding condition."

What it means: You won't be asked to make repairs—but they'll adjust the price to account for anything they find.

Why it matters: "As-is" sounds simple, but combined with uncapped repair credits, it can result in significant price reductions after you've already committed.

Red flag level: Moderate. Understand that "as-is" doesn't mean "no deductions."

Liquidated Damages Clause

What it says: "If Seller fails to close, Seller shall pay Buyer [specific amount] as liquidated damages."

What it means: If you change your mind or can't close for some reason, you owe them money—sometimes thousands of dollars.

Why it matters: Life happens. Job changes, family emergencies, or simply finding a better option shouldn't cost you a financial penalty that's disproportionate to any actual harm to the buyer.

Red flag level: High if the amount is substantial. Look for reasonable, proportionate terms.

Confidentiality/Non-Disclosure Clause

What it says: "Seller agrees not to disclose the terms of this agreement to any third party."

What it means: You can't tell anyone—including other potential buyers, real estate professionals, or even a consultant—about the offer.

Why it matters: This prevents you from comparison shopping or getting a second opinion.

Red flag level: Extremely high. Why would a legitimate company prevent you from seeking advice?r

Red Flags That Should Make You Pause

Beyond specific clauses, watch for these warning signs:

Pressure to Sign Quickly

"This offer expires in 24 hours." "We have other properties we're looking at." "The market is shifting—this is your best chance."

Legitimate companies understand that selling your home is a major financial decision. Aggressive pressure tactics often signal that they don't want you to think too hard about the terms.

Vague or Missing Fee Disclosures

If you can't get a clear answer about total fees, repair credit caps, or closing costs, that's a problem. Reputable iBuyers provide detailed net proceeds estimates upfront.

No Physical Inspection Before the Offer

Some companies make offers based solely on algorithms and photos, then conduct inspections afterward. The gap between the initial offer and the final price after inspection adjustments can be substantial.

This isn't necessarily a dealbreaker, but go in with eyes open: the first number is preliminary.

Earnest Money That Favors the Buyer

In traditional transactions, earnest money (a deposit showing good faith) typically comes from the buyer. Some "we buy houses" contracts minimize or eliminate earnest money from their side while imposing strict penalties on you.

Contract Language You Don't Understand

If you can't explain a clause in plain English, that's a signal to slow down. You're not expected to be a legal expert, but you should understand what you're agreeing to.

A Checklist for Evaluating Any Cash Offer

Before signing, work through this framework:

Financial Clarity

[ ] What is the offer price?

[ ] What is the service fee (percentage and dollar amount)?

[ ] Is there an inspection contingency? If so, is the repair credit capped?

[ ] What are the estimated closing costs?

[ ] What are my estimated net proceeds (offer minus all deductions)?

Contract Terms

[ ] Is there an assignment clause? Am I comfortable with it?

[ ] What are my obligations if I want to cancel?

[ ] What are the buyer's obligations if they want to cancel?

[ ] Is there a confidentiality clause preventing me from seeking advice?

[ ] What is the proposed closing timeline?

Company Verification

[ ] Is the company properly licensed in my state (if required)?

[ ] Can I find reviews or verify their track record?

[ ] Have I received clear answers to my questions?

Comparison

[ ] Have I compared this net proceeds estimate to what I might net from a traditional sale?

[ ] Do I understand the tradeoffs I'm making for speed/convenience?

When a Cash Sale Might Make Sense

Despite the cautions above, cash offers serve legitimate purposes. Consider this path if:

Speed is genuinely critical: Job relocation, financial hardship, inherited property, or divorce situations sometimes make a fast close more valuable than a higher price.

Your home needs significant repairs: If your property requires major work, a cash buyer who purchases "as-is" might actually net you more than investing in repairs and selling traditionally.

You've exhausted traditional options: A home that's sat on the market for months might benefit from a different approach.

The key is making an informed decision—not a pressured one.

Frequently Asked Questions

How much do iBuyers typically charge in fees?

Service fees generally range from 5% to 6% of the sale price, though some companies have charged higher percentages in certain markets. [2] Always request a written breakdown before committing. Remember that repair credits and closing costs come off separately, so the total deductions often exceed the stated service fee.

Can I negotiate with a "we buy houses" company?

Sometimes, though it depends on the company and your leverage. The initial offer is often a starting point, especially if you have competing offers or a strong position. However, many cash buyers operate on thin margins and have limited flexibility. Don't assume the first number is final, but don't expect dramatic changes either.

What happens if I sign and then change my mind?

Review your contract's cancellation terms carefully before signing. Many cash-buyer contracts include liquidated damages clauses or other penalties for seller cancellation. Some offer a brief review period; others lock you in immediately. Understanding your exit options upfront is essential.

Should I have an attorney or real estate professional review the contract?

Having someone knowledgeable review the contract before you sign is generally wise, especially if you're unfamiliar with real estate transactions. A second set of eyes can catch unfavorable terms you might miss. Be wary of any company that discourages you from seeking outside advice.

How do I compare a cash offer to what I'd get selling traditionally?

Focus on net proceeds, not offer price. Estimate what your home might sell for on the open market, subtract likely commissions, closing costs, and any repairs you'd need to make, then compare that number to the cash buyer's net proceeds estimate. Factor in the value of your time and the certainty of a guaranteed sale.

Taking the Next Step

Reading this guide is a solid start. But evaluating an actual offer—with real numbers and binding contract language—benefits from a second opinion.

If you've received a cash offer and want someone to walk through the details with you, consider scheduling a consult. A quick review before you sign can clarify whether the terms align with your goals—or whether you should keep looking.

Request a consult to review your offer summary before signing.

About This Guide

This article was prepared to help Sacramento-area homeowners make informed decisions when evaluating cash purchase offers. The information draws on publicly available industry analyses, consumer protection guidance, and standard real estate practice knowledge. For advice specific to your situation, consult with a qualified professional.

Tavon Willis is a California-licensed real estate salesperson (DRE #02095751) serving the Greater Sacramento area, including Elk Grove and surrounding communities. With a focus on homeownership education and helping clients navigate complex decisions, Tavon provides guidance rooted in transparency and client advocacy—not pressure.

Cited Works

[1] Federal Trade Commission — "What to Know About iBuyers." https://consumer.ftc.gov/articles/selling-your-home

[2] Bankrate — "iBuyer fees: What to expect when selling to an iBuyer." https://www.bankrate.com/real-estate/ibuyer-fees/

[3] MarketWatch — "The hidden costs of selling to an iBuyer." https://www.marketwatch.com/picks/guides/real-estate/ibuyer-companies/