Buying your first home in Sacramento follows a predictable sequence—one that thousands of buyers complete every year across the region. The challenge isn't complexity; it's knowing what happens at each stage before you get there.

This roadmap breaks down the entire process from financial prep through closing day, with specific attention to California's escrow system, Sacramento-area market dynamics, and the documents you'll encounter along the way. By the end, you'll understand how a Loan Estimate differs from a Closing Disclosure, why inspection contingencies protect you, and how local factors like Mello-Roos taxes and utility providers affect your monthly costs.

Stage 1: Get Your Finances Ready Before You Shop

Most first-time buyers want to start touring homes immediately. That approach creates problems.

Your first step is understanding what you can realistically afford—not the maximum a lender approves, but the monthly payment that works within your actual budget. Sacramento-area property taxes, insurance premiums, and HOA dues can add hundreds to your monthly housing cost, and these amounts don't appear in the mortgage payment a lender initially quotes.

What to do now:

Pull your credit reports from all three bureaus at AnnualCreditReport.com (the only federally authorized free source) [1]

Calculate your debt-to-income ratio by adding monthly debt payments and dividing by gross monthly income

Estimate your total down payment and closing costs (closing costs in California typically run 2-5% of the purchase price) [2]

Research down payment assistance through the California Housing Finance Agency (CalHFA) and the Sacramento Housing and Redevelopment Agency (SHRA), which offers programs specifically for Sacramento County residents [3] [4]

Sacramento-specific costs to factor in:

Property taxes: Sacramento County property taxes generally run around 1.1-1.2% of assessed value annually, though this varies by location. [5]

Mello-Roos taxes: Many newer Sacramento developments—particularly in Elk Grove, Natomas, Folsom, and Rancho Cordona—include Mello-Roos Community Facilities District taxes. These are additional property taxes that fund infrastructure like roads, parks, and schools in newer communities. Mello-Roos can add $2,000-$6,000+ annually to your tax bill depending on the district. Always ask whether a property falls within a Mello-Roos district before making an offer. [6]

Utility considerations: Much of Sacramento County is served by the Sacramento Municipal Utility District (SMUD) rather than PG&E. SMUD rates are typically lower than PG&E's, which can meaningfully reduce monthly costs compared to neighboring areas served by PG&E. Verify which utility provider serves any home you're considering. [7]

Feeling stuck on the numbers? Request a first-time buyer consultation to talk through your specific situation.

Stage 2: Secure Your Pre-Approval (Not Just Pre-Qualification)

Pre-qualification and pre-approval are different processes with different weight in the market.

Pre-qualification is a quick estimate based on information you provide to a lender verbally. Pre-approval means the lender has verified your income, assets, employment history, and credit through documentation. In Sacramento's market, sellers and listing agents expect pre-approval letters with offers—a pre-qualification letter typically won't make your offer competitive. [8]

The Loan Estimate document

Within three business days of applying for a mortgage, your lender must provide a Loan Estimate—a standardized three-page form required by federal law. [9] This document shows:

Your estimated interest rate and monthly payment

Projected closing costs itemized by category

How much cash you'll need at closing

Whether your rate is locked, and for how long

Compare Loan Estimates from multiple lenders. The Consumer Financial Protection Bureau recommends getting at least three quotes—rates and fees vary significantly between lenders, even for identical borrowers. [9]

Loan types to discuss with your lender:

| Loan Type | Minimum Down Payment | Key Consideration |

| Conventional | 3-5% | Often requires PMI below 20% down |

| FHA | 3.5% | More flexible credit requirements |

| VA | 0% | For eligible veterans and service members [10] |

| CalHFA Programs | Varies | State-specific assistance options [3] |

Timeline consideration:

Pre-approval letters typically remain valid for 60-90 days. If your home search extends beyond that window, you'll need updated documentation and a fresh letter. Plan your search timeline accordingly.

Questions about which loan type fits your situation? Schedule a call to discuss your options.

Stage 3: Define Your Search Criteria (The Sacramento Way)

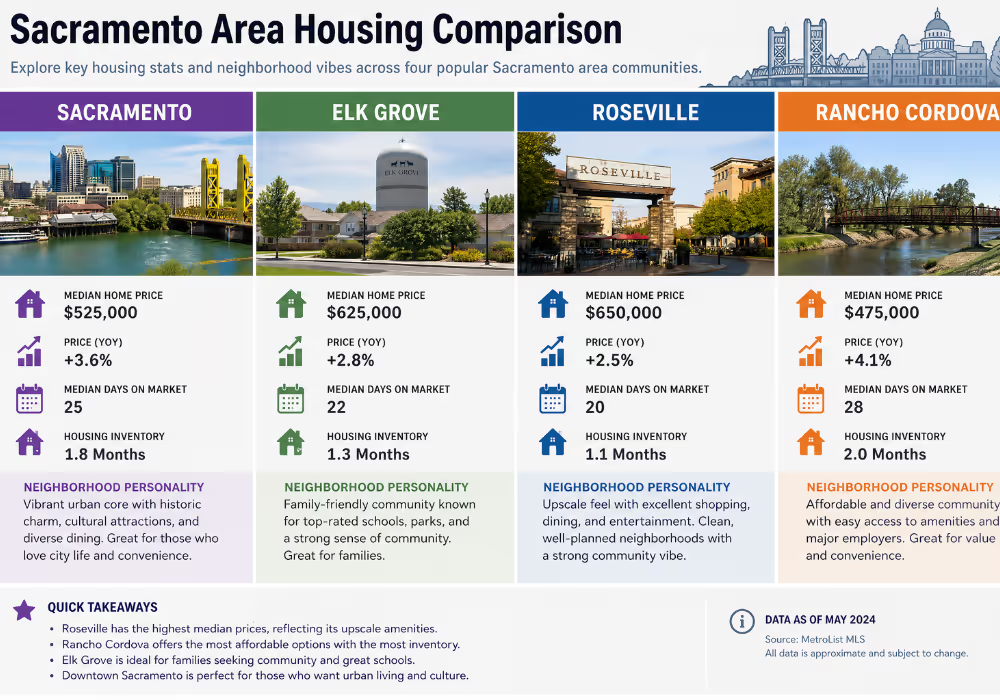

Sacramento sprawls across multiple corridors, each with distinct commute patterns, housing stock, and development characteristics. Your search strategy should account for these differences before you tour your first home.

Commute-driven search radius

Sacramento buyers frequently underestimate how commute patterns should shape their search. Consider these factors:

Highway 50 corridor (Folsom, El Dorado Hills) versus I-80 corridor (Roseville, Rocklin) versus Highway 99 corridor (Elk Grove, South Sacramento)

Peak commute times to your workplace—drive the route during rush hour before committing to an area

Light rail accessibility if public transit matters to your daily routine [11]

New construction versus resale in Sacramento

Sacramento has significant new construction activity, particularly in Elk Grove, Natomas, Rancho Cordova, and the Folsom/Roseville areas. [12]

New construction considerations:

Builder incentives may include rate buy-downs, closing cost credits, or upgrade packages

Timelines range from 4-12+ months depending on the build stage when you purchase

Energy efficiency standards are typically higher than older homes (California Title 24 requirements)

HOA fees and Mello-Roos taxes are common in newer developments—factor both into your monthly budget

Consider bringing your own buyer's agent to the sales office; builder representatives work for the builder, not you

Resale considerations:

Faster closing timelines (typically 30-45 days)

Established landscaping and neighborhoods

May require more immediate maintenance or updates

More negotiating room on price in some market conditions

Older homes may have lower or no Mello-Roos taxes

HOA prevalence in Sacramento

Many Sacramento neighborhoods built after 1990 have homeowners associations. HOA dues in the Sacramento region commonly range from $50-$300+ monthly depending on amenities. [13] Request the HOA's CC&Rs (Covenants, Conditions, and Restrictions) before making an offer—these documents govern everything from exterior paint colors to parking rules to rental restrictions.

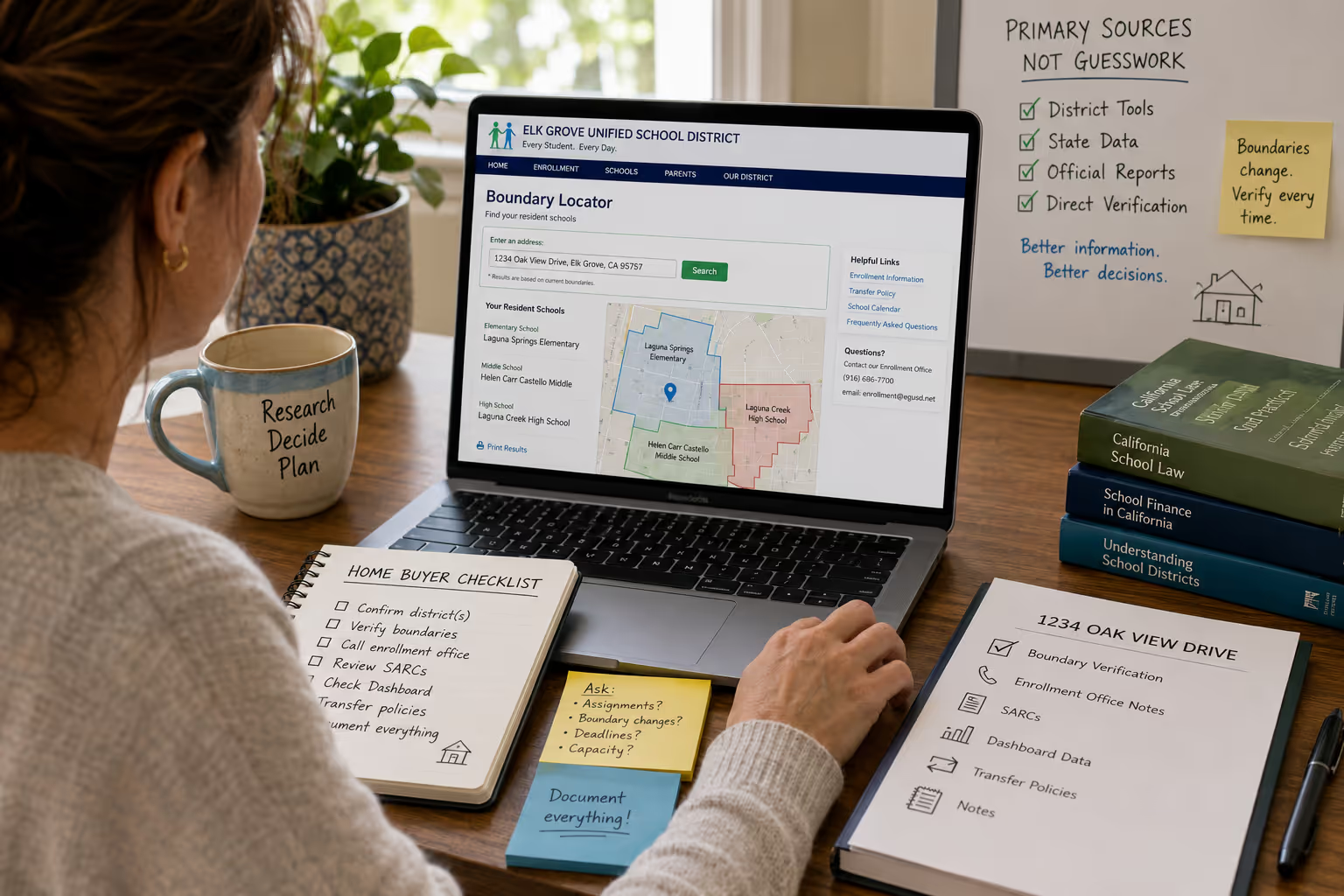

How to research neighborhoods without relying on opinions:

Check commute times using Google Maps during typical work hours

Review school district boundaries through official district websites (Sacramento City Unified, Elk Grove Unified, San Juan Unified, etc.)

Look up flood zone status through FEMA's flood map service [14]

Verify which utility providers serve the address (SMUD vs. PG&E for electricity)

Research any special tax districts through the Sacramento County Assessor's office [5]

Need help building your search criteria? Connect with a local agent who can walk through the tradeoffs.

Stage 4: Tour Homes and Make an Offer

Once financing is lined up and search criteria are defined, the touring phase often moves faster than first-time buyers expect.

What to bring to showings:

Your pre-approval letter (don't share it until you're making an offer)

A checklist of must-haves versus nice-to-haves

Your phone for photos and notes

Questions about the age of major systems (roof, HVAC, water heater)

Making an offer in California

California uses standardized purchase agreement forms created by the California Association of REALTORS®. [15] Your offer will include:

Purchase price and how you're paying (financing type, down payment amount)

Earnest money deposit (typically 1-3% of purchase price in Sacramento)

Contingencies protecting your right to back out under specific conditions

Proposed closing timeline (30-45 days is standard for financed purchases)

What's included in the sale (appliances, fixtures, window coverings)

Critical contingencies to understand:

Inspection contingency: Gives you the right to hire a professional inspector, review findings, and either negotiate repairs, request credits, or withdraw from the contract. California's standard contingency period is typically 17 days but can be negotiated. [15]

Appraisal contingency: Protects you if the home appraises below your offer price. This matters because lenders won't finance more than the appraised value.

Loan contingency: Allows you to exit if your financing falls through despite good-faith efforts to secure approval.

Removing contingencies is a negotiating tool in competitive situations. However, think carefully before waiving the inspection contingency on your first home—the potential cost of undiscovered problems typically outweighs the competitive advantage.

Ready to start touring? Request a buyer consultation to build your strategy.

Stage 5: Navigate the Escrow Process (California-Specific)

California handles real estate closings differently than many other states. Here, escrow companies—not attorneys—manage the closing process.

Escrow is a neutral third party that holds your earnest money, coordinates document signing, ensures all contract conditions are met, and facilitates the transfer of funds and title. [16] The escrow company works for both parties and has no stake in whether the transaction closes.

Your Sacramento escrow timeline (typical 30-day close):

| Days | What's Happening |

| 1-3 | Escrow opens, earnest money deposited |

| 3-10 | Home inspection scheduled, seller disclosures reviewed |

| 7-14 | Appraisal ordered and completed |

| 10-17 | Inspection negotiations resolved, contingencies removed |

| 14-21 | Loan underwriting, conditions cleared |

| 21-25 | Final loan approval, closing documents prepared |

| 25-28 | Final walkthrough, signing appointment scheduled |

| 30 | Funding and recording—you get keys |

Note: In competitive Sacramento sub-markets, appraisal scheduling can sometimes cause delays. Build a few days of buffer into your timeline expectations.

Key documents during escrow:

Transfer Disclosure Statement (TDS): California law requires sellers to disclose known material facts about the property's condition. [17] Read this document thoroughly.

Natural Hazard Disclosure: Required disclosure covering flood zones, fire hazard areas, earthquake fault zones, and other natural hazards affecting the property. [17]

Preliminary Title Report: Shows ownership history and any liens, easements, or encumbrances on the property. Review for anything unexpected before closing.

The Closing Disclosure

At least three business days before closing, your lender must provide the Closing Disclosure—a five-page document showing your final loan terms and all closing costs. [9]

Compare this carefully to your original Loan Estimate. Certain changes (like a significantly different interest rate or loan product) can restart the three-day waiting period.

Items to verify on your Closing Disclosure:

Loan amount, interest rate, and monthly payment match expectations

Closing costs align reasonably with your Loan Estimate (some variance is normal; large discrepancies need explanation)

Prepaid items (property taxes, insurance, HOA dues) are calculated correctly

Your cash-to-close amount is accurate

Stage 6: Close and Get Your Keys

Closing day in California typically happens at the escrow office or through a mobile notary service.

What to bring:

Valid government-issued photo ID

Certified or cashier's check for your closing funds (or wire transfer confirmation—verify wiring instructions by phone using a known number, not email links)

Any outstanding documentation your lender requested

What happens at signing:

You'll sign the promissory note (your promise to repay the loan), deed of trust (which secures the loan against the property), and various federal and state disclosures. Plan for 60-90 minutes of signing.

After you sign:

Your loan funds, the transaction "records" with the Sacramento County Recorder's Office, and the home officially transfers to you. Recording typically happens the same day or the next business day. [18]

Then you get your keys.

Common First-Time Buyer Mistakes in Sacramento

Learning from others' missteps saves stress and money.

Shopping before getting pre-approved. You'll either look at homes outside your budget or lose competitive offers because your financing isn't verified.

Ignoring HOA documents and Mello-Roos disclosures. In newer Sacramento developments, HOA rules affect everything from parking to landscaping to rental restrictions. Mello-Roos taxes can add several hundred dollars monthly to your housing cost. Request and read both before committing.

Skipping the inspection to be competitive. Even in a busy market, the inspection contingency protects you from expensive surprises. Negotiate the timeline if necessary, but understand what you're giving up if you waive it entirely.

Draining savings for the down payment. Keep reserves for moving costs, immediate repairs, and unexpected expenses. Lenders also verify you have some savings remaining after closing.

Making major purchases during escrow. A new car purchase or furniture bought on credit can change your debt-to-income ratio and derail your loan approval. Wait until after closing.

Walking into new construction sales offices without representation. Builder sales representatives work for the builder. Consider bringing your own buyer's agent before your first visit to a new development.

What to Expect With Your Budget in Sacramento

While prices fluctuate with market conditions, understanding general ranges helps you set realistic expectations.

Sacramento-area first-time buyers often target homes in the $350,000-$550,000 range, though this varies significantly by neighborhood, condition, and whether you're considering new construction or resale. [19]

Your monthly housing payment includes:

Principal and interest on your mortgage

Property taxes (collected monthly through your lender's escrow account or paid separately)

Homeowners insurance

Private mortgage insurance (if applicable)

Mello-Roos taxes (if applicable)

HOA dues (if applicable)

A common guideline suggests keeping total housing costs below 28-30% of gross monthly income, though individual circumstances and local cost-of-living factors may shift what works for your situation. [20]

Call to Action

Buying your first home in Sacramento is achievable with the right preparation. The process has clear steps, and knowing what's coming at each stage removes most of the uncertainty.

Ready to start your homebuying journey? Request a consultation to talk through your timeline, budget, and questions. No pressure—just clarity on your next steps.

Frequently Asked Questions

How long does it take to buy a house in Sacramento from start to finish?

Most first-time buyers spend 2-4 months from initial pre-approval to closing, though this varies based on market conditions and how quickly you find the right property. The escrow period itself typically runs 30-45 days once your offer is accepted. New construction purchases can extend significantly longer—sometimes 6-12 months—depending on where the home is in the build process when you commit.

What credit score do I need to buy a home in Sacramento?

Minimum credit score requirements depend on loan type. Conventional loans typically require 620 or higher, FHA loans allow scores as low as 580 with 3.5% down, and VA loans have no federally mandated minimum though most lenders prefer 620+. [10] Higher credit scores generally qualify for better interest rates, which significantly affects your monthly payment over the life of the loan.

How much should I save for a down payment and closing costs?

Plan for 3-20% of the purchase price for your down payment (depending on loan type) plus 2-5% for closing costs. [2] California assistance programs through CalHFA and SHRA may reduce upfront requirements for eligible buyers. [3] [4] For a home priced around $450,000, total upfront costs might range from $25,000-$45,000 with a low down payment loan, before accounting for any assistance programs.

What are Mello-Roos taxes and how do they affect my payment?

Mello-Roos taxes are additional property taxes that fund infrastructure and services in Community Facilities Districts, typically newer developments. They're common in Sacramento-area communities like Elk Grove, Natomas, and Rancho Cordova. Mello-Roos can add $2,000-$6,000+ annually to your property tax bill depending on the district. These taxes are disclosed during the purchase process, but ask early—they significantly affect your total monthly housing cost. [6]

Should I buy new construction or a resale home in Sacramento?

Neither option is universally better—the right choice depends on your priorities. New construction offers current energy efficiency standards, builder incentives (potentially including rate buy-downs), and lower near-term maintenance needs, but typically involves longer timelines and often includes both HOA fees and Mello-Roos taxes. Resale homes close faster and may offer more negotiating flexibility, but could require updates or repairs. Evaluate both based on your budget, timeline, and what tradeoffs matter most to you.

About This Guide

This first-time homebuyer roadmap reflects current California real estate practices, federal lending requirements, and Sacramento-area market conditions. Information is drawn from official sources including the Consumer Financial Protection Bureau, California Department of Real Estate, California Housing Finance Agency, Sacramento Housing and Redevelopment Agency, and California Association of REALTORS® guidelines. For guidance specific to your situation, consult with a licensed real estate professional and mortgage lender familiar with Sacramento transactions.

Cited Works

[1] Federal Trade Commission — "Free Credit Reports." https://www.annualcreditreport.com/

[2] Consumer Financial Protection Bureau — "Buying a House." https://www.consumerfinance.gov/owning-a-home/

[3] California Housing Finance Agency — "Homebuyer Programs." https://www.calhfa.ca.gov/

[4] Sacramento Housing and Redevelopment Agency — "Homeownership Programs." https://www.shra.org/

[5] Sacramento County Assessor — "Property Tax Information." https://finance.saccounty.gov/Tax/

[6] California State Controller's Office — "Mello-Roos Community Facilities Districts." https://www.sco.ca.gov/

[7] Sacramento Municipal Utility District — "About SMUD." https://www.smud.org/

[8] California Association of REALTORS® — "Standard Forms." https://www.car.org/

[9] Consumer Financial Protection Bureau — "Loan Estimate Explainer." https://www.consumerfinance.gov/owning-a-home/loan-estimate/

[10] U.S. Department of Veterans Affairs — "VA Home Loans."

https://www.va.gov/housing-assistance/home-loans/

[11] Sacramento Regional Transit — "Light Rail." https://www.sacrt.com/

[12] California Department of Real Estate — "Real Estate Law." https://www.dre.ca.gov/

[13] U.S. Department of Housing and Urban Development — "Buying a Home." https://www.hud.gov/topics/buying_a_home

[14] FEMA — "Flood Map Service Center." https://msc.fema.gov/

[15] California Association of REALTORS® — "Purchase Agreement Forms." https://www.car.org/

[16] California Department of Real Estate — "Escrow Law." https://www.dre.ca.gov/

[17] California Civil Code — "Transfer Disclosure Requirements." https://leginfo.legislature.ca.gov/

[18] Sacramento County Clerk/Recorder — "Recording Services." https://clerkrecorder.saccounty.gov/

[19] California Association of REALTORS® — "Housing Market Data." https://www.car.org/

[20] Consumer Financial Protection Bureau — "Debt-to-Income Calculator." https://www.consumerfinance.gov/